Jarque-Bera normality test has significant p-values even when there is skewness and kurtosis. Does that mean test is infering data distribution is approximately normal?

Asked

Active

Viewed 2.4k times

5

-

9a significant p-value for the Jarque-Bera test indicates that you can **reject** the null hypothesis of normality ... – Ben Bolker Jan 26 '14 at 17:19

1 Answers

8

You may have misunderstood something about hypothesis testing or maybe about goodness-of-fit tests, or perhaps specifically about the "Jarque-Bera" test*.

Note that you reject when the p-value is small, when happens when the skewness and kurtosis differ from their expected values under normality.

The test statistic is of the form (from page 1 of Bowman and Shenton's paper):

$$\frac{n}{6} S^2 + \frac{n}{24} (K-3)^2\,,$$

where $S$ is the sample skewness and $K$ is the sample kurtosis (i.e. $K-3$ is 'excess kurtosis')

The null hypothesis is of normality, and rejection of the hypothesis (because of a significant p-value) leads to the conclusion that the distribution from which the data came is non-normal.

The test is specifically looking for skewness and kurtosis that is different from that of the normal (it squares the standardized deviations and sums them) and will tend to be significant when skewness and kurtosis deviating from the values at the normal are present.

Which is to say - when you get a significant test statistic with this test, it's explicitly because the sample skewness or kurtosis (or both) are different from what you expect to see with a sample from normal distribution.

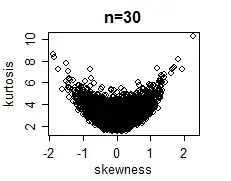

Take care, however -- the asymptotic approximation on which the test is based comes in only very slowly (see the image near the bottom of this answer; also see here and here for some additional points). I wouldn't rely on it without simulating the distribution of the test statistic unless $n$ is a good deal larger than say 100.

Here's an example of the joint distribution in normal samples at n=30 (simulated values):

-- as you see, not at all close to bivariate normal.

*(The development of the test precedes their 1980 paper; it shouldn't be named for them. D'Agostino & Pearson (1973), and then Bowman & Shenton (1975) were there well before for example, and the latter discussed the relevant issues in more detail (including the slow convergence and the shape of the joint distribution in small samples - though their diagrams seem as if they may contain an error), but one can readily see that the idea of basing a goodness of fit test on skewness and kurtosis together comes even earlier than those prior papers.)

Glen_b

- 257,508

- 32

- 553

- 939

-

1+1 Re the footnote: You are aware of [Stigler's Law of Eponymy](http://en.wikipedia.org/wiki/Stigler%27s_law_of_eponymy), are you not? – whuber Jan 27 '14 at 00:01

-

@whuber indeed. I do what I can to mitigate it nonetheless. Bowman and Shenton deserve proper recognition at the least. – Glen_b Jan 27 '14 at 00:04

-

4In my experience, citing Jarque and Bera usually flags that the authors are economists or econometricians. Occasionally it can be useful as flagging to discerning readers that there is lack of awareness in a paper of mainstream statistics literature. – Nick Cox Jan 27 '14 at 00:53

-

@NickCox That was certainly my impression about 20 years ago, but lately it seems references to Jarque and Bera are becoming more widespread even among statisticians, while awareness of Bowman and Shenton's work (and more especially, on what it tells us about using the test 'as is') seem to be disappearing. I put it down to widespread availability of "Jarque-Bera" tests in packages now ... many people never read papers. – Glen_b Jan 27 '14 at 00:59

-

-

Thanks Glen. Am I right to say if I use 5% significance I will still see some Skewness even test say normal, p-value < 0.05? and skewness = 0 means normal even though there is some kurtosis? – sigirisetti Jan 27 '14 at 05:12

-

sigrisetti I don't understand your question, it seems a bit jumbled. Note that failure to reject does *not* mean you have normality. You can be confident that exact normality is essentially never true. (Further, if you sample from a normal distribution, you can observe skewness and kurtosis in the sample.) – Glen_b Jan 27 '14 at 07:04