Step 1. To answer "Final Question"

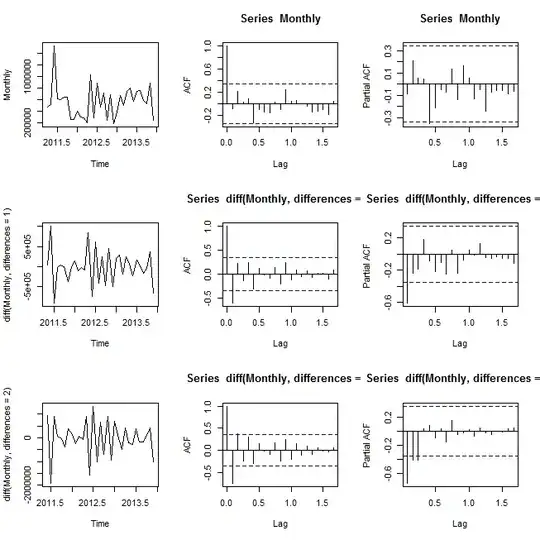

Expecting to find correct order of difference to achieve stationary.

Some Result of test for stationary on monthly times series only.

Dickey fuller

KPSS test

Phillips–Perron test

If required i can provide test result for the any order difference.

> urdfTest(Monthly, lags=1, type = c("nc","c","ct"), doplot = TRUE)

Title:

Augmented Dickey-Fuller Unit Root Test

Test Results:

Test regression none

Call:

lm(formula = z.diff ~ z.lag.1 - 1 + z.diff.lag)

Residuals:

Min 1Q Median 3Q Max

-526683 -135297 24570 176578 1078796

Coefficients:

Estimate Std. Error t value Pr(>|t|)

z.lag.1 -0.08703 0.09829 -0.885 0.383219

z.diff.lag -0.61315 0.15711 -3.903 0.000521 ***

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 329300 on 29 degrees of freedom

Multiple R-squared: 0.4195, Adjusted R-squared: 0.3794

F-statistic: 10.48 on 2 and 29 DF, p-value: 0.0003761

Value of test-statistic is: -0.8854

Critical values for test statistics:

1pct 5pct 10pct

tau1 -2.62 -1.95 -1.61

> urkpssTest(Monthly, type = c("mu","tau"), lag = c("short","long","nil"), use.lag = NULL, doplot = TRUE)

Title:

KPSS Unit Root Test

Test Results:

Test is of type: mu with 3 lags.

Value of test-statistic is: 0.0986

Critical value for a significance level of:

10pct 5pct 2.5pct 1pct

critical values 0.347 0.463 0.574 0.739

> urppTest(Monthly, type = c("Z-alpha","Z-tau"), model = c("constant","trend"), lags = c("short","long"),use.lag = NULL, doplot = TRUE)

Title:

Phillips-Perron Unit Root Test

Test Results:

Test regression with intercept

Residuals:

Min 1Q Median 3Q Max

-397594 -251734 26252 144863 954417

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 6.169e+05 1.183e+05 5.215 1.27e-05 ***

y.l1 -8.733e-02 1.857e-01 -0.470 0.641

---

Signif. codes: 0 ‘***’ 0.001 ‘**’ 0.01 ‘*’ 0.05 ‘.’ 0.1 ‘ ’ 1

Residual standard error: 290200 on 30 degrees of freedom

Multiple R-squared: 0.007322, Adjusted R-squared: -0.02577

F-statistic: 0.2213 on 1 and 30 DF, p-value: 0.6415

Value of test-statistic, type: Z-alpha is: -39.5851

aux. Z statistics

Z-tau-mu 5.2378