I'm wondering about the monotonic quantile transformation in case of a t distribution. First, for explanation, lets consider a normal distribution:

\begin{align*} f(l | \mu , \sigma ^2)=\frac{1}{\sigma \sqrt{2 \pi}} e^{-\frac{(l-\mu)^2}{2 \sigma ^2}} \end{align*}

A quantile at $\alpha$ can be calculated by

$Quantile_\alpha=\mu + \sigma \Phi^{-1}(\alpha)$

so e.g. lets say $\mu = -0.0000615$ and $\sigma=0,0145$, the 0,95 quantile of the normal distribution is 1,644854 so

$Quantile_{0.95}=-0.0000615+0,0145*1,644854=0.02379$

So now for the t distribution, I use the following notation:

\begin{align*} f(l|\nu ,\mu ,\beta) = \frac{\Gamma (\frac{\nu+1}{2})}{\Gamma (\frac{\nu}{2}) \sqrt{\pi \nu} \beta} \left(1+\frac{1}{\nu}\left(\frac{l - \mu}{\beta}\right)^2 \right)^{\text{$-\frac{1+\nu}{2}$}} \end{align*}

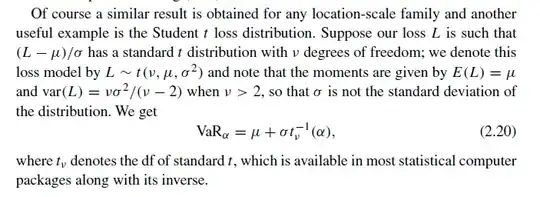

now, I have this from a book:

ignore the "VaR", it only sais, we focus on the right side of the distribution.

And now I am not really sure about the quantile computation anymore. I think my $\beta$ is the $\sigma^2$ right?

So is this correct: $Quantile_{\alpha}^{t}=\mu + \beta t_\nu^{-1}(\alpha) $

or this: $Quantile_{\alpha}^{t}=\mu + \sqrt{\beta} t_\nu^{-1}(\alpha) $

As an example, I have the following values:

$\mu=-0.0012827$

$\beta=0.009891722$

$\nu = 3.34331$

and therefore $t_{3.34331}^{-1}(0.95)=2.258039$

now, is

$Quantile_{0.95}^{t}=-0.0012827+0.009891722*2.258039=0.02105319$

or

$Quantile_{0.95}^{t}=-0.0012827+\sqrt{0.009891722}*2.258039=0.2232954$

correct?

Mh, I am not sure, since I am confused about the $\sigma^2$ they use, but 0.2232954 CANNOT be empirical correct, so it MUST be the 0.021? Where is my mistake?

the book: Alexander J. McNeil, Rüdiger Frey, Paul Embrechts: Quantitative Risk Management 2005 page 40.