I am trying to test this property of pareto distribution: Let f(x) be a pareto distribution

$$ f(x)=\alpha \frac{x_m^\alpha}{x^{\alpha+1}} $$

so we have the cdf that is

$$ CDF(x)=\int_{x_m}^{x}\alpha \frac{t_m^\alpha}{t^{\alpha+1}}dt=1-\frac{x_m^\alpha}{x^\alpha} $$

then the probability that $x>x_0$ is

$$ P(x>x_0)=1-CDF(x)=\frac{x_m^\alpha}{x^\alpha} $$

and so we have

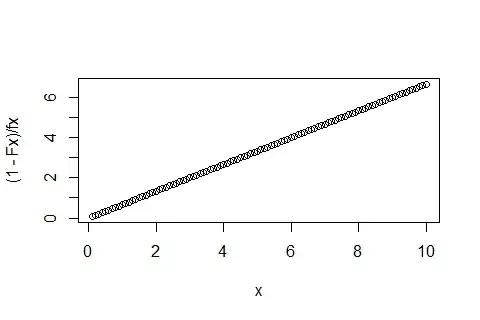

$$ \frac{P(x>x_0)}{f(x)}=\frac{x}{\alpha} $$

Now i am trying to test it with R.

library(PtProcess)

dd<-rpareto(10000,1.5,0.01)

cdf<-ecdf(dd)

df<-density(dd)

ff<-(1-cdf(df$x))/df$y

If i plot ff

plot(df$x,ff)

I do not obtain the correct straight line. I guess that this is due at the way density() and ecdf() works. I need this form of the test (an a posteriori evaluation of fd and cdf) in order to perform the same test on a sample of data of unknown orgin. I guess that i need a way to binning the ecdf() function in the same way as hist() is the binning version of density.

So my question is:

- Does there exist an equivalent binned function of ecdf() as hist() is the binned function of density()?

- or can I simulate ecdf() with hist()?