Indeed, the "skew-normal family" has exploded in membership (the wikipedia article does not attest to this). So, let's consider the mother of them all, that has probability density function

$$f_X(x) = \frac{2}{\omega}\phi\left(\frac{x-\xi}{\omega}\right)\Phi\left(\alpha \left(\frac{x-\xi}{\omega}\right)\right)$$

where $\phi()$ is the standard normal pdf and $\Phi()$ the standard normal cdf. $\xi$ is the location parameter, $\omega$ is the scale parameter, and $\alpha$ is the skew parameter.

Closed-form solutions for the ML estimator do not exist. Method-of-Moments estimator provides closed forms as follows, assuming that all three parameters are non-zero (obviously if $\omega$ and/or $\xi$ are zero, then the steps below are simplified):

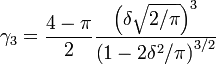

1) Obtain a MoM estimate $\hat \delta$ by solving for $\delta$ the expression for the skewness of the distribution,

using the estimated sample skewness coefficient $\hat \gamma_3$.

2) Obtain an estimate $\hat \alpha$ using

$$\delta = \frac {\alpha}{\sqrt {(1+\alpha^2)}} \implies \hat \alpha = \frac {\hat \delta}{\sqrt{1-\hat \delta^2}}$$

3) Obtain a MoM estimate $\hat \omega$ by solving for $\omega$ the expression for the variance,

$$\hat \sigma^2_x = \omega^2\cdot \left(1-\frac{2\hat \delta^2}{\pi}\right)$$

using the sample variance and the estimated $\delta$ derived in the previous step

3) Obtain a MoM estimate $\hat \xi$ by solving for $\xi$ the expression for the mean of the distribution,

$$\hat \mu_x = \xi + \hat \omega \hat \delta\sqrt {2/\pi}$$

using the sample mean and the previous estimates.

And don't forget to propagate estimation error in this sequential procedure, as regards the estimator variance.