Is there a formal statistical test to test if process is a white noise?

Asked

Active

Viewed 1.4k times

10

-

1against what alternative ? – user603 Feb 11 '11 at 15:03

2 Answers

14

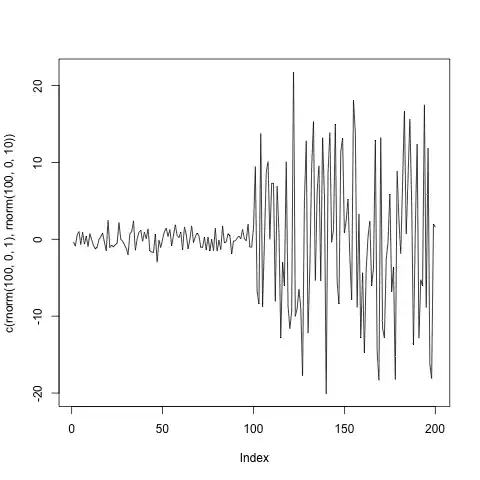

In time-series analysis usually Ljung-Box test is used. Note though that it tests the correlations. If the correlations are zero, but variance varies, then the process is not white noise, but Ljung-Box test will fail to reject the null-hypothesis. Here is an example in R:

> Box.test(c(rnorm(100,0,1),rnorm(100,0,10)),type="Ljung-Box")

Box-Ljung test

data: c(rnorm(100, 0, 1), rnorm(100, 0, 10))

X-squared = 0.4771, df = 1, p-value = 0.4898

Here is the plot of the process:

Here is more discussion about this test.

-

Ouliers in the error series will "deflate the ACF" thus yielding an ALICE IN WINDERKlAND effect. All ACF's are subject to this thus one must ensure no anomalies – IrishStat Mar 21 '11 at 23:44

0

The R library hwwntest (Haar Wavelet White Noise test) seems to work pretty well. It offers a number of functions. It does require the amount of data to be a power of 2.

hywavwn.test() seems to work the best for me.

> hywavwn.test(rnorm(128, 0, 1))

Hybrid Wavelet Test of White Noise

data:

p-value = 0.542

> hywavwn.test(rnorm(128, 0, 10))

Hybrid Wavelet Test of White Noise

data:

p-value = 1

Sven Hohenstein

- 6,285

- 25

- 30

- 39

Clem Wang

- 101

- 1