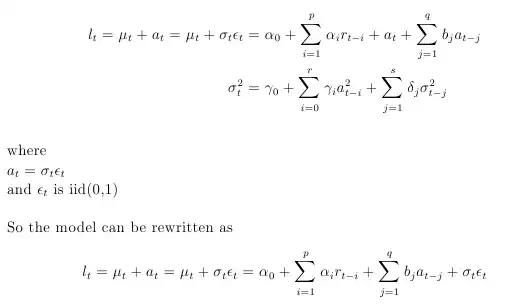

For my variable $l_t$ I want to use an ARMA(p,q)-GARCH(r,s). So the mean equation follows an ARMA(p,q) and the conditional volatility is modelled by a GARCH(r,s). Is my notation correct?

Asked

Active

Viewed 631 times

1

Stat Tistician

- 2,113

- 4

- 29

- 54

-

The GARCH filter does not depend on information at time $t$. You need to start your counter for $a_{t-i}$ at 1. Please see my answer [here](http://stats.stackexchange.com/a/41514/8141). – tchakravarty Feb 14 '15 at 09:14