The Secretary problem has an algorithm for fixed N and immediate accept/reject (that is, reject reject ... accept one, stop). There are several variants; in mine, secretaries or samples come from a real-valued source Xj, payoff is from best-so-far not last, and each sample costs $ c:

maximize payoff = Xbestsofar - c * Nsample

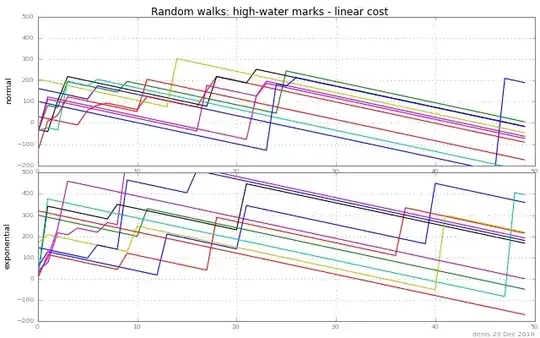

Here's a picture of random walks of this kind: either go up to a high-water mark (new maximum) of X1 X2 ..., or down c:

Can anyone point me to stop-or-keep-looking rules for optimal stopping for problems like this ? Perhaps one could combine two kinds of rule:

sample at least ..., take the best after that (Secretary problem)

stop when the peak - current exceeds some Δ (Allaart)

As @whuber points out, one needs some model of the distribution of the samples to define the problem. This I don't have. Nonetheless, statisticians must have looked at problems of this kind -- sequential sampling, sequential design of experiments, optimal stopping, optimal learning ? Then please help me rephrase my question to ask for a tutorial on ...

Added links 29Dec, thanks @James; readers please extend —

Optimal stopping

Hill, Knowing when to stop

2009, 3p, excellent

Allaart,

Stopping the maximum of a correlated random walk with cost for observation

2004, 12p

(Sorry to keep changing this — trying to converge to a standard formulation.)