In Bayesian statistics one uses a 'flat' prior distribution for

a parameter in the absence of knowledge or opinion about about

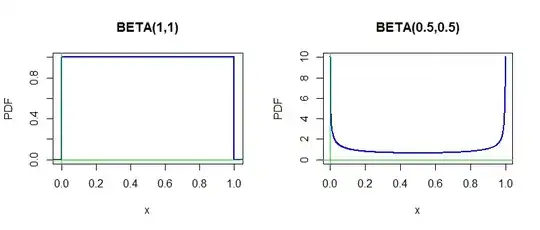

the parameter value. When the parameter is binomial success probability $p$ it may seem natural to use either a uniform prior $\mathsf{Beta}(\alpha=1,\beta=1)\equiv\mathsf{Unif}(0,1)$ or even the "bathtub shaped"

prior $\mathsf{Beta}(.5, .5).$

par(mfrow=c(1,2))

hdr1 = "BETA(1,1)"

curve(dbeta(x,1,1), -.05,1.05, ylab="PDF",

col="blue", lwd=2, xaxs="i", n=10001, main=hdr1)

abline(v=0, col="green2"); abline(h=0, col="green2")

hdr2 = "BETA(0.5,0.5)"

curve(dbeta(x,.5,.5), 0,1, ylab="PDF", col="blue", lwd=2,

ylim=c(0,10), n=1001, main=hdr2)

abline(v=0, col="green2"); abline(h=0, col="green2")

par(mfrow=c(1,1))

The purpose of using a flat prior distribution may be for the posterior

distribution on the parameter to be mainly due to the data.

For example, if the prior is $\mathsf{Beta}(1,1)$ and the data

show $x=23$ successes in $n=50$ trials, then the likelihood

is proportional to $p^x(1-p)^{n-x} = p^{23}(1-p)^{27}.$

Thus

the posterior distribution is $\mathsf{Beta}(24, 28)$ and

a 95% Bayesian credible interval for $p$ is $(0.33,\,0.600,$

which agrees numerically with a frequentist 95% frequentist Agresti-Coull

confidence interval $(0.33,\,0.60)$ to two decimal places.

qbeta(c(.025,.975),24,28)

[1] 0.3293001 0.5965812

p.est = 25/54

p.est + qnorm(c(.025,.975))*sqrt( p.est*(1-p.est)/54 )

[1] 0.3299707 0.5959553

Note: The distribution $\mathsf{Beta}(.5,.5)$ is called a Jeffreys prior. It can be argued that it is less informative as a prior than is $\mathsf{Beta}(1,1).$ The interval estimate $(0.33, 0.60)$ from this prior distribution is sometimes used as a frequentist CI:

qbeta(c(.025,.975),23.5,27.5)

[1] 0.3273505 0.5971336