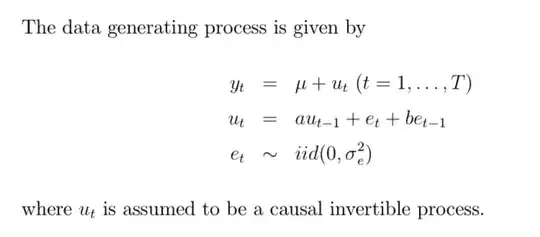

The $u_t$ is an ARMA (1,1) process. Here you have an ARMA(1,1) error term for the random variable $y_t$. A process with an ARMA(1,1) error terms will have long-run mean of $\mu$. Therefore, your sample mean of $y_t$ is $\sum_{t=1}^T y_t = \hat \mu$. You get the long-run variance of $\hat \mu$, by applying a central limit theorem for MA processes. To do this, you could rewrite $y_t$ as a function of $\mu$ and lagged $e_t$'s. Then, assuming that the conditions for the CLT are satisfied,

$$\sqrt{T}(\bar{y}_T - \mu) \overset{d}{\to} N\left(0, \sum_{h = -\infty}^{\infty} \gamma_h\right)$$

where $\gamma_h$ is the h-th order autocovariance term. Some additional maths reveals that $\sum_{h = -\infty}^{\infty} \gamma_h = \sigma_{\epsilon}^2 \left(\frac{1-b}{1-a}\right)^2$.