Let’s say

$X_1$ ~ $uni(0,1)$

$X_2$ ~ $uni(0,1)$

$X_3$ ~ $uni(0,1)$

And

$Y=0.1X_1+0.3X_2+0.6X_3$

What’s the $F(Y)$ (i.e., CDF)?

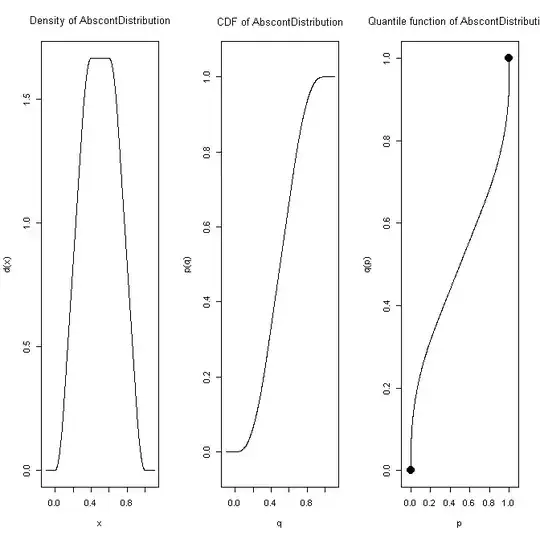

Let’s say

$X_1$ ~ $uni(0,1)$

$X_2$ ~ $uni(0,1)$

$X_3$ ~ $uni(0,1)$

And

$Y=0.1X_1+0.3X_2+0.6X_3$

What’s the $F(Y)$ (i.e., CDF)?

It is not one of the common named distributions, but the distr package in R can help you explore it:

library(distr)

d <- 0.1*Unif() + 0.3*Unif() + 0.6*Unif()

plot(d)