I would like to do time series decomposition, but the error term has a serial autocorrelation at the end and I am freaking out because I have really no idea what to do with that.

How I did it?

I tried to use ucm command in Stata but I faced a lot of problems, always having some errors.

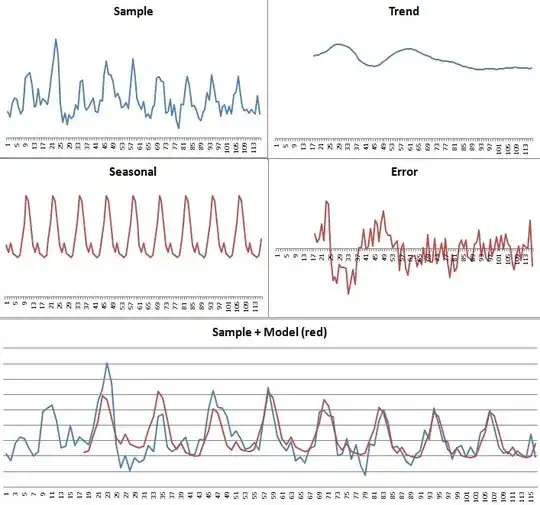

Finally only the command ucm TOTAL, seasonal(12) iterate(11) from(e(b)) worked but it gave me only the trend component. later when I was trying to do the further components I had millions of problems in my Stata, so I simply calculated the seasonal component in Excel and then simply the

Trend component from Stata * Seasonal Component from Excel = Predicted model

and then Sample - Model = Error.

And Breusch-Godfrey test in Stata shows autocorrelation :

Chi2 Prob>chi2

26,261 0,0000

Can someone please correct my messy thinking and help me to do the decomposition of time series or what should i do with the fact that error is autocorrelated?

my output: