Suppose we have the following model for the variable $V_5$: $$V_5 = \prod_{k=1}^5(e^{\mu + 0.2X_k}+0.05e^{0.05Y_i - 0.00125}), X_i,Y_i\sim N(0,1)$$

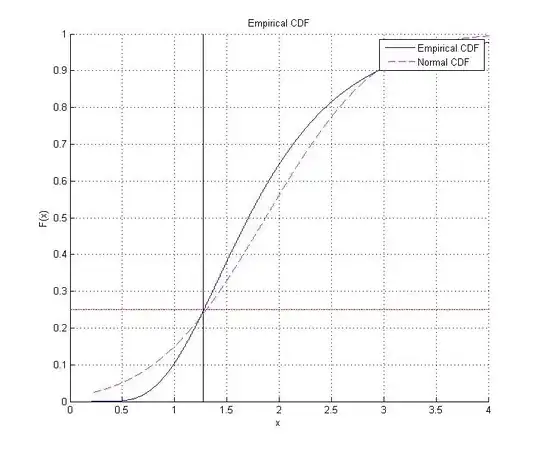

What I wish to do is to solve the problem $\min_{\mu}\{F_{V_5}(1.2763) = 0.25\}$. By performing $10^7$ simulations for the value of $V_5$, I find that this optimal $\mu$ is somewhere in the neighborhood of $0.06$ with small deviations in the value of $F$, i.e. I find that if $\mu = 0.06$ then $F_{V_5}(1.2673) = 0.2484$ or $0.2487$ or other very similar values in that area, but never exactly $0.25$. If I change the value of $\mu$ to either larger or smaller than $0.06$ then the value of $F$ starts diverging farther away from $0.25$. In addition, the empirical CDF is clearly not normal, but it does approximate a normal with mean the sample mean of $V_5$ and $\sigma^2$ the sample variance of $V_5$ rather closely at exactly the point $(1.2763 , 0.25)$ as you can see in the picture below (and I'm not sure that this is a coincidence or not):

Now my question is, how can I prove that $\mu = 0.06$ is indeed the optimal value that we are looking for? When I asked my professor, he said that I should construct a confidence interval, but since we didn't get $\mu$ from an estimation or anything (I found it by rather eyeballing the problem), that leaves me with the idea of a confidence interval for the probability $F_{V_5}(1.2763)$, which I have no clue how to construct.

Any suggestion or different solution to the problem is most welcome.