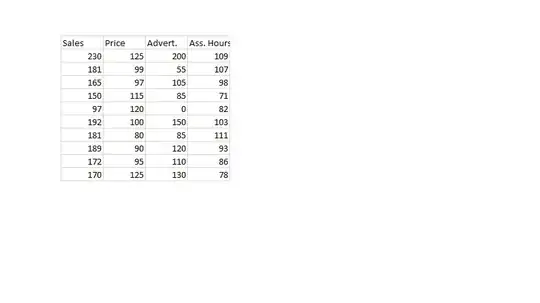

suppose that we have following data

i have done covariance matrix and eigenvalue decomposition

>> means=mean(X);

>> centered=X-repmat(means,10,1);

>> covariance=(centered'*centered)/(9);

>> [V,D]=eig(covariance);

>> [e,i]=sort(diag(D),'descend');

>> sorted=V(:,i);

e

e =

1.0e+03 *

3.8861

0.4605

0.1162

0.0465

>> sorted

sorted =

0.5080 0.5042 0.3747 -0.5893

0.0090 -0.6091 0.7930 -0.0092

0.8560 -0.3490 -0.2747 0.2647

0.0955 0.5030 0.3941 0.7633

i have calculated also percentage distribution

(e./sum(e))*100

ans =

86.1796

10.2125

2.5776

1.0303

for instance i want to choose first two,because in sum they have more then 96% of total variance,now please how can i continue for factor analysis?matlab commands also visual help will be very good,according to this answer

Steps done in factor analysis compared to steps done in PCA

i was confused,so please for given concrete numerical example,how can i continue,not just definitions,i need concrete numerical steps.thansk in advance

EDITED : because i have choose first two eigenvector,i have done PCA also

factors=sorted(:,1:2)

factors =

0.5080 0.5042

0.0090 -0.6091

0.8560 -0.3490

0.0955 0.5030

>> PCA=X*factors

PCA =

299.5739 24.8602

150.1380 65.5846

183.9319 36.7606

156.7749 11.6325

58.1864 17.0585

236.6723 35.3584

176.0291 68.7008

208.4237 45.3761

190.6039 33.7278

206.2131 3.4430

how can i calculate loadings?how can i do orthogonal rotations?